Last week, the domestic steel market continued its downward trend, with prices falling further and more sharply. While some areas in northern China saw modest improvements in trading activity, most steel products across the country experienced widespread declines. With weakening demand, ongoing drops in raw material costs, and increasing financial pressure, both forward and spot prices hit their lowest levels since 2013, with no clear signs of a temporary recovery. Market sentiment turned increasingly pessimistic, as traders became more willing to cut prices aggressively in an attempt to move inventory.

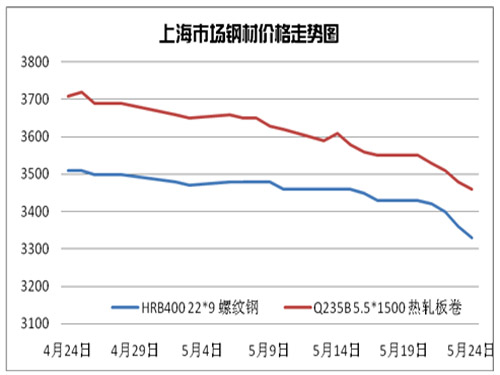

In Shanghai, steel prices fell significantly last week. Construction steel dropped by 100 yuan per ton, with mainstream prices for three-grade rebar in Xicheng and Rizhao ranging between 3,330–3,350 yuan per ton. Hot-rolled coil prices fell by 90 yuan per ton, with popular brands like Rizhao and Shagang quoted at 3,450–3,480 yuan per ton. Cold-rolled coil prices also dropped by 80 yuan per ton, with Wuhan Iron and Steel and Benxi’s cold roll prices at 4,480–4,500 yuan per ton.

The author believes that several key factors are driving the accelerated decline in steel prices:

First, steel demand has weakened significantly. Industries such as real estate, automotive, and construction machinery have seen sluggish demand, which has been a major driver of price declines. Recent economic data suggests that the domestic economy is not expected to recover quickly, directly impacting steel demand. According to HSBC's May 2013 manufacturing PMI data, the initial reading was 49.6, below the 50.4 in April and the lowest in seven months. The manufacturing output index also fell to 51.0 from 51.1 in April, marking the lowest level in three months. Analysts note that weak domestic and external demand contributed to this drop, increasing downside risks for the second quarter. As temperatures rise and the rainy season begins in the south, steel demand is expected to shrink further, forcing traders to compete on price to secure limited orders.

Second, raw material prices have continued to fall. As of May 24th, the ex-factory price of 66% iron ore in Tangshan dropped to 800–830 yuan per ton, down 20 yuan from the previous week. In Qingdao, 63.5% iron ore was priced at 915–925 yuan per wet ton, down 15 yuan. At Beilun port, 63% Brazilian fines were also quoted at 915–925 yuan per wet ton, down 20 yuan. Steel mills remain cautious, with low inquiries and weak transactions. Meanwhile, carbon billet prices in Tangshan fell to 3,060 yuan per ton, while 20MnSi billets dropped to 3,180 yuan per ton, down 20 yuan from the previous week. The rapid decline in raw materials has significantly reduced cost support, leading to further pessimism in the market.

Third, there has been little progress in reducing steel production. Although many steel mills have announced maintenance plans this month, actual production cuts have not been significant. According to the China Iron and Steel Association, crude steel output from major enterprises in the first half of May rose by 2.71% month-on-month, reaching 1.748 million tons daily. National estimates show a 3.02% increase compared to the previous period, with daily output hitting a record high for the same period over ten years. This indicates that production cuts have not been effective, and steel mills are still producing at high levels, putting more pressure on the market.

Fourth, financial pressure remains severe. After a prolonged period of price declines, many companies are facing losses. Traders are struggling with tight capital flows, and some are nearing the breaking point. Maintaining low inventory has become the norm, reducing the role of traders as market stabilizers. This not only slows resource movement but also increases inventory and financial burdens. As the month-end approaches, traders are forced to cut prices further to free up capital and prepare for next month’s orders.

Overall, with no immediate improvement in demand, combined with heavy inventory and financial pressures, and the continued decline in raw material prices, the steel market is under significant downward pressure. The bearish sentiment is strong, and further price declines are likely in the near term.

Last week, the domestic steel market continued its downward trend, with prices falling further and more sharply. While some areas in northern China saw modest improvements in trading activity, most steel products across the country experienced widespread declines. With weakening demand, ongoing drops in raw material costs, and increasing financial pressure, both forward and spot prices hit their lowest levels since 2013, with no clear signs of a temporary recovery. Market sentiment turned increasingly pessimistic, as traders became more willing to cut prices aggressively in an attempt to move inventory.

In Shanghai, steel prices fell significantly last week. Construction steel dropped by 100 yuan per ton, with mainstream prices for three-grade rebar in Xicheng and Rizhao ranging between 3,330–3,350 yuan per ton. Hot-rolled coil prices fell by 90 yuan per ton, with popular brands like Rizhao and Shagang quoted at 3,450–3,480 yuan per ton. Cold-rolled coil prices also dropped by 80 yuan per ton, with Wuhan Iron and Steel and Benxi’s cold roll prices at 4,480–4,500 yuan per ton.

The author believes that several key factors are driving the accelerated decline in steel prices:

First, steel demand has weakened significantly. Industries such as real estate, automotive, and construction machinery have seen sluggish demand, which has been a major driver of price declines. Recent economic data suggests that the domestic economy is not expected to recover quickly, directly impacting steel demand. According to HSBC's May 2013 manufacturing PMI data, the initial reading was 49.6, below the 50.4 in April and the lowest in seven months. The manufacturing output index also fell to 51.0 from 51.1 in April, marking the lowest level in three months. Analysts note that weak domestic and external demand contributed to this drop, increasing downside risks for the second quarter. As temperatures rise and the rainy season begins in the south, steel demand is expected to shrink further, forcing traders to compete on price to secure limited orders.

Second, raw material prices have continued to fall. As of May 24th, the ex-factory price of 66% iron ore in Tangshan dropped to 800–830 yuan per ton, down 20 yuan from the previous week. In Qingdao, 63.5% iron ore was priced at 915–925 yuan per wet ton, down 15 yuan. At Beilun port, 63% Brazilian fines were also quoted at 915–925 yuan per wet ton, down 20 yuan. Steel mills remain cautious, with low inquiries and weak transactions. Meanwhile, carbon billet prices in Tangshan fell to 3,060 yuan per ton, while 20MnSi billets dropped to 3,180 yuan per ton, down 20 yuan from the previous week. The rapid decline in raw materials has significantly reduced cost support, leading to further pessimism in the market.

Third, there has been little progress in reducing steel production. Although many steel mills have announced maintenance plans this month, actual production cuts have not been significant. According to the China Iron and Steel Association, crude steel output from major enterprises in the first half of May rose by 2.71% month-on-month, reaching 1.748 million tons daily. National estimates show a 3.02% increase compared to the previous period, with daily output hitting a record high for the same period over ten years. This indicates that production cuts have not been effective, and steel mills are still producing at high levels, putting more pressure on the market.

Fourth, financial pressure remains severe. After a prolonged period of price declines, many companies are facing losses. Traders are struggling with tight capital flows, and some are nearing the breaking point. Maintaining low inventory has become the norm, reducing the role of traders as market stabilizers. This not only slows resource movement but also increases inventory and financial burdens. As the month-end approaches, traders are forced to cut prices further to free up capital and prepare for next month’s orders.

Overall, with no immediate improvement in demand, combined with heavy inventory and financial pressures, and the continued decline in raw material prices, the steel market is under significant downward pressure. The bearish sentiment is strong, and further price declines are likely in the near term.Import Brand Bearings,Self Aligning Ball Bearing,Needle Roller Bearing,Linear Bearing

Shanghai Yi Kai Cheng bearing Co., LTD , https://www.ykchbearing.com